[Estimated reading time: 28 minutes]

Today is 18 August 2022. As I started writing this essay, the U.S. was deep in the the season for political campaigns meant to inform and persuade the electorate before the midterm elections—called the “midterms” because they occur in the middle of a U.S. president’s four-year term—are held to elect people to the U.S. Congress and state and local public offices. The U.S. will hold its next midterm election on 8 November 2022, after a string of primary elections and run-offs to narrow the field of candidates.

Obtaining information about beliefs, opinions, and voting preferences before the midterm elections is crucial for many reasons. This information can guide campaign strategy. Also, campaign donors can receive signals from this information about candidates’ worthiness for continuing financial or moral support. This information can further focus the mission for campaign workers and can validate the effort behind their commitment to candidates. Moreover, when candidates display public support, voter attention is drawn to candidates and their deeper bios.

In this blog posting, I focus on the use of information markets in place of survey methods for identifying candidate preferences of the electorate.1 Information markets operate similarly to commodity and financial futures markets, except that the commodity traded in contracts is information, not a physical good. Information markets trade contracts for propositions about whether events will occur and when.

The mission of this blog posting is to describe concepts and processes to apply commodity and financial futures markets to structure information markets for estimating candidate preferences of the electorate. In the remainder of this posting, I offer some examples of information markets for demonstrating their applications to diverse questions that also could be answered using survey methods. But, first, to set the stage, I contrast the two approaches—survey methods v information markets—for estimating beliefs about the outcome of a Pennsylvania political race for the U.S. Senate that will be decided in a November 2022 midterm.

Fetterman v Oz: Two Approaches to Estimating Voter Preferences

The 2022 Pennsylvania midterm race for U.S. Senate is garnering national attention (see, e.g., Glueck (2022)). John Fetterman, a Democrat, is pitted against Mehmet Oz, a Republican. Fetterman serves as the 34th lieutenant governor of Pennsylvania. He was mayor of Braddock, Pennsylvania, from 2006 to 2019. Oz is a Turkish–American television personality, author, professor emeritus at Columbia University, and retired cardiothoracic surgeon. He is the first Muslim to be nominated by either major political party for U.S. Senate. The outcome of this race could have profound impact on the balance of power in the U.S. Senate and stands as a test of the efficacy of endorsements for office by former U.S. president Donald Trump. I describe two alternatives for estimating beliefs about the outcome of the Fetterman v Oz race for for Senate: one uses survey methods and the other uses of information markets.

Estimation Using Survey Methods

(Walter et al., 1999)17 August 2022 Preference

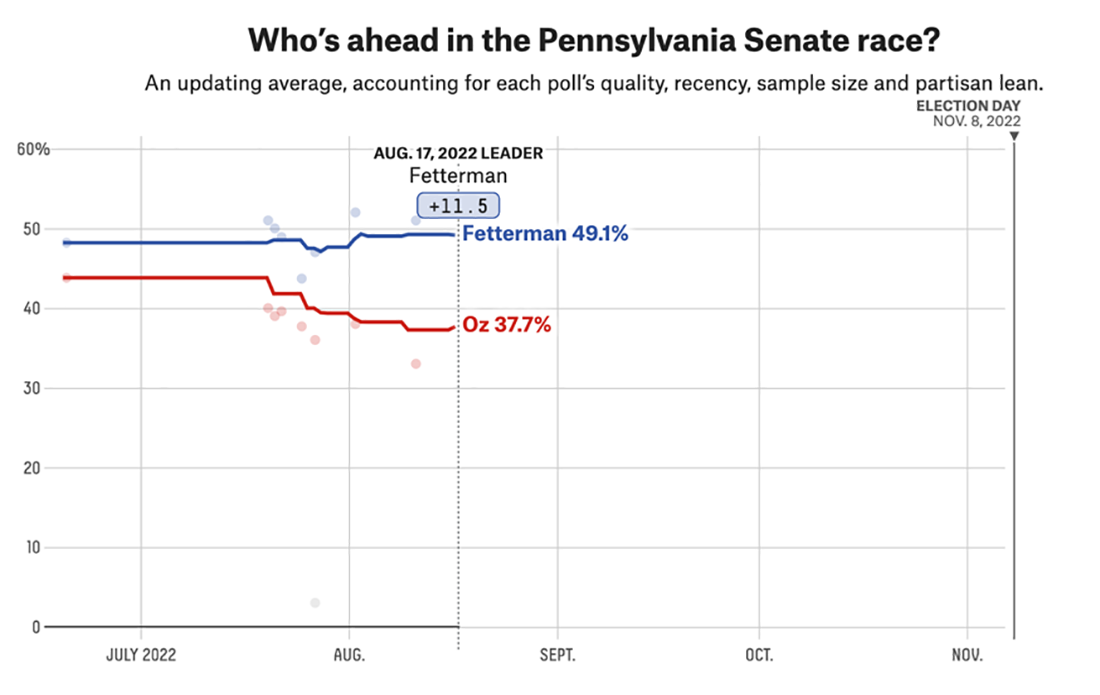

As of 17 August 2022, respondents favored Fetterman by 11.1% over Oz (see Figure 1). A weighted average percent favoring a candidate from a number of polls is the basis of this estimate (Silver, 2008).2

Figure 1: Lead by Fetterman over Oz in averaged survey findings in fivethirtyeight.com on 17 August 2022.

(Image from Best et al. (2022).)

Methods for surveys are richly varied and well-documented (see, e.g., workflows by Fink (2015), Kelley, et al. (2003), and Walter et al. (1999) ), and I will not restate them here. In brief, a sample of respondents is recruited from a population of interest to answer questions. Estimates of responses in the population are inferred from responses in the sample, with a band of confidence around the estimates reflecting the possibility of differences between the population parameters and the estimates from the sample. Analysts attempt to account for response and non-response errors and biases in the estimates.

Survey Project Management

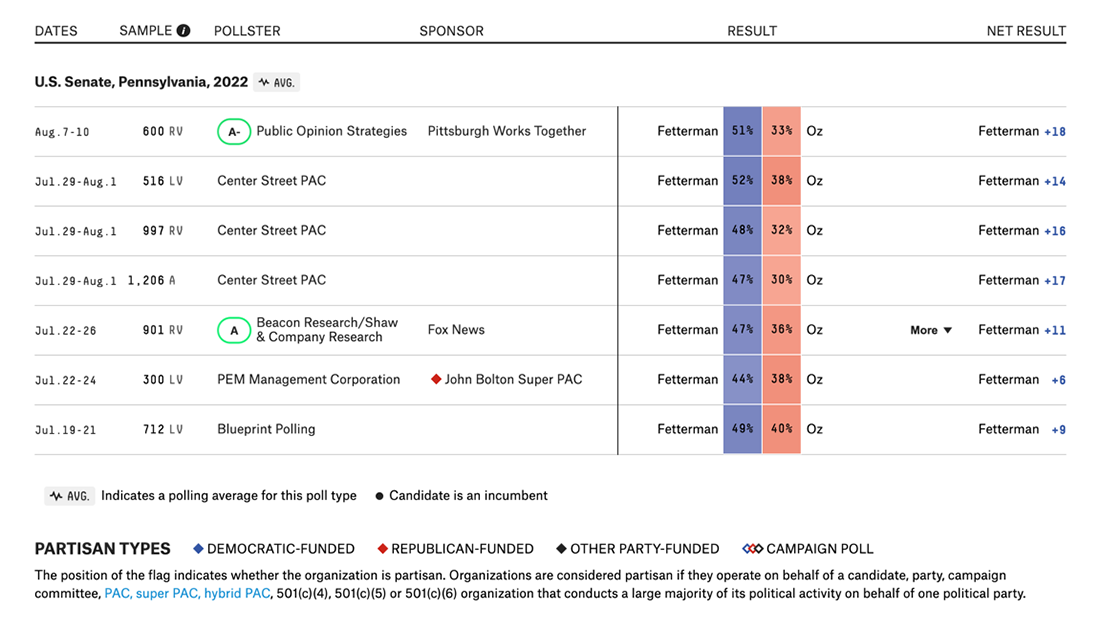

In the fivethirtyeight.com estimates multiple independent surveys of the relative preferences for the two candidates were averaged over different survey vendors and time periods to provide a meta-estimate of the status of the Fetterman v Oz race. (see Figure 2 for examples of selected surveys in the fivethirtyeight.com analysis). Each one of the surveys averaged by fivethirtyeight.com represents a separate project with a work plan for collecting, organizing, analyzing, and reporting derived information. Logistical impediments and added costs in using surveys can result from the complexity and cycle time necessary to complete survey projects and from the need to report survey findings to fit time-sensitive strategic information needs and time-limited media attention.

Figure 2: Selected findings from Fetterman v Oz survey findings averaged by fivethirtyeight.com

(Image from Best et al. (2022).)

Implementation of professionally–produced surveys can require extensive budgeting for, among other elements, survey design, staffing, respondent recruitment, and perhaps establishing effective incentives to motivate to survey responses each time a survey is conducted. Increasing the the size of the respondent sample can balloon costs as it can require design of complex survey questions that branch the flows of questions conditional on criteria for segmenting respondents (e.g., “If you are married and a homeowner, skip to Q23.”). Implementation of survey methods can draw on significant resources as a campaign progresses.

Estimation Using an Information Market

The Fetterman v Oz Market

The basis of an information market is a contract for a written proposition, the truth of which is validated at a specific future date. Contract prices range between zero and $1. The price the buyer of a contract is willing to pay represents the buyer’s belief in the fulfillment of the proposition when the market closes at a future date.

On 18 August 2022, PredictIt, a project of Victoria University, located in Wellington, New Zealand (PredictIt, 2022b), had been running an information market for 181 days to obtain bets about the outcome of the Fetterman v Oz race, which is a comparison similar to the assessment conducted by fivethirtyeight.com that is in Figure 1. Criteria for assessing the fulfillment of the proposition in the PredictIt market are reproduced in Figure 3.

![*Rules for judging the outcome of* "Which party will win the U.S. Senate election in Pennsylvania in 2022?" *in PredictIt political market.* <br> (Image from Best et. al [-@best2022a.] on 17 August 2011 @ 12:19 pm.)](https://davidpassmore.net/blogd/img/infomarkets/Fetterman_rules.png)

Figure 3: Rules for judging the outcome of “Which party will win the U.S. Senate election in Pennsylvania in 2022?” in PredictIt political market.

(Image from Best et. al (2022.) on 17 August 2011 @ 12:19 pm.)

Trading in the PredictIt Exchange

Here is how trading in the Fetterman v Oz information futures market works in PredictIt:

- A buyer may purchase as many contracts as desired.

- Individual contract prices vary from zero to $1.

- Owners of contracts may either sell or hold their contracts.

- The prices of “Yes” and “No” contracts always are complementary. That is, The “Yes” and “No” prices must sum to $1.

- A buyer may offer any price; the seller may accept or reject any price.

- The market price paid for a contract is conceptualized as the probability that the proposition will eventuate by market closing.

- In this particular binary (“Yes” or “No”) proposition, a buyer

selects one of four options to purchase a contract -

- for Fetterman to win (meaning Oz will lose)

- for Fetterman to lose (meaning Oz will win)

- for Oz to win (meaning Fetterman will lose)

- for Oz to lose (meaning Fetterman will win)

- for Fetterman to win (meaning Oz will lose)

Markets other than for binary outcomes are available. For example,

markets allowing selection from a range of outcomes are possible.

PredictIt closed on 24 May 2022 a market in which participants bought

contracts on the percentage of the popular vote cast in favor of John

Fetterman in the 2022 Pennsylvania Democratic primary election for the U.S.

Senate on 7 May 2022 (see PredictIt (2022a) for prices at the close of the

market). Other complex forms of markets can include joint outcomes.

Although PredictIt does not offer such a market, participants could

construct propositions that include, for example, the likelihood of

favoring a particular gubernatorial candidate and favoring Fetterman

for the Senate.

18 August 2022 Share Prices

Shown in Figure 4 are the market prices on 17 August

2022 for the proposition, Which party will win the U.S. Senate

election

in Pennsylvania in 2022?. The market price for 17 August

indicated a strong belief that Fetterman would beat Oz in the race by the

closing date for the market, much stronger than in the difference

estimated by survey methods (refer again to Figure

1).

![*Market price for* "Which party will win the U.S. Senate election <br> in Pennsylvania in 2022?" *in PredictIt political market.* <br> (Image from Best et. al [-@best2022a.] on 17 August 2011 @ 12:19 pm.)](https://davidpassmore.net/blogd/img/infomarkets/Fetterman_daymarket.png)

Figure 4: Market price for “Which party will win the U.S. Senate election

in Pennsylvania in 2022?” in PredictIt political market.

(Image from Best et. al (2022.) on 17 August 2011 @ 12:19 pm.)

Estimates based on survey methods and information markets are not entirely equivalent. For instance, The survey-based estimates are averaged from responses to questions that generally request a preference among candidates. The estimate from the information market requires the prediction of which candidate will win the race, conditional on information aggregated by the market participant from various points of information about candidate prospects. For the most part, the survey-based approaches rely on which candidate you like, while the estimates from the information market focus on who will win, regardless of who the market participant favors. Respondents to surveys generally have no pecuniary stake in the outcome of the race. At the same time, information market participants placed money (albeit a small stake) on their bet.

This market has a “winner–take–all” reward. When the market closes, holder of a contract for the winning share will receive $1, and the holder of the losing share will receive nothing. Buyers and sellers can engage in a variety of trading strategies based on information they discover about the race:

- A buyer could bet on a winner to make money when the market closes.

If so, a strategy is to get in the market while the price is low and

hold it as it soars (you hope and, indeed, bet) to market closing.

- A buyer could bet on a candidate with a current low market price if

the buyer believes that a candidate’s fortunes will turn just enough

to raise an acceptable return on investment—“buy low, sell high.”

- Or, maybe a buyer bets on the winner of this race, even if the buyer

are unconcerned about the political outcome as a hedge against a

risky bet in another market.

-A buyer could engage in arbitrage because the market has not reacted quickly to changes in information about the race or is just not paying attention to information that signals a shift in fortunes. This approach involves buying when the buyer believes that the market price is artificially low or high. The buyer could reap a quick reward by selling initially undervalued contracts at the market price to newly informed investors. When the market artificially is too high, the buyer could buy contracts for a discount from sellers holding contracts with high-than-rational price who are eager to exit the market before experiencing more price erosion.

Price-Volume Chart

Displayed in Figure 5 is a plot following the market share price and volume over a 90-day period. The trajectory of the market price shows how beliefs about the outcome of the Fetterman v Oz race changed over time. Notice that beliefs that Oz would win the race in the month after Fetterman announced a health condition (a stroke). Then, Fetterman reversed this trend and continued to widen the gap with Oz.

Tracked in each vertical bar on the plot in Figure 5 is the volume of shares traded in each of the 90 days. High volume days indicate interest in the proposition represented in the contract. A surge in trading occurred on 15 June, perhaps as concerns about Fetterman’s health began to wane. The volume of trades rose near the date Fox News reported that Fetterman agreed with a plan to cut the prison population by one-third (Chasmar, 2022). A surge in trading happened, raising Fetterman’s market price, around the date that Breitbart syndicated information about Fetterman’s call for heavy fines against airlines for flight cancellations (Dixon-Hamilton, 2022).

My attributions of reasons behind volume surges in the Fetterman v Oz market are ad hoc and speculative. However, a serious campaign analyst could track and explain how campaign activities, media buzz, candidate gaffs and peccadilloes, and buzz about candidates affect beliefs about the outcome of a political race.

![*90-day price-volume plot for* "Which party will win the U.S. Senate election in Pennsylvania in 2022?" *in PredictIt political market.* <br> (Image from Best et. al [-@best2022a.].)](https://davidpassmore.net/blogd/img/infomarkets/Fetterman_vol_price.png)

Figure 5: 90-day price-volume plot for “Which party will win the U.S. Senate election in Pennsylvania in 2022?” in PredictIt political market.

(Image from Best et. al (2022.).)

Commodity Futures and Information Markets Are in the Same Family

General Features of Commodities Futures Markets

Commodities

A futures contract is:

a legal agreement to buy or sell a particular commodity asset, or security at a predetermined price at a specified time in the future. Futures contracts are standardized for quality and quantity to facilitate trading on a futures exchange. (Hayes, 2021)

For example, a buyer might purchase a contract for delivery of 5,000 bushels of No. 2 Yellow Corn (AG Commodities, 2022) on the following March 1 for $3.82 per bushel. The buyer of a futures contract takes on the obligation to buy and receive the underlying asset when the futures contract expires. The seller of the futures contract is taking on the obligation to provide and deliver the underlying asset at the expiration date.

Buyers of futures contracts typically are investors, not producers. Buyers usually sell their interest in a commodity to a producer before it is delivered.3 A clearing corporation brokers trading of futures contracts by acting as a single counter-party to every transaction and by guaranteeing the completion and creditworthiness of all transactions. PredictIt is the clearing corporation for contracts such as the Fetterman v Oz contract in the PredictIt information market.

Commodities include mostly raw, unprocessed goods that are bought based on price alone in large quantities for future processing. The U.S. government defines commodities in the 1936 Commodity Exchange Act (Legal Information Institute, 2022). Commodities are classified into three major categories: agriculture, energy, and metals. The most popular futures markets for food are for meat, wheat, and sugar. Most energy futures are in oil and gasoline markets. Metals using futures markets include gold, silver, and copper. The 1936 Act also governs financial products (e.g., future values of interest rates, currencies, stock indexes, bonds, or equity and debt options) as commodities. Buyers of food, energy, and metal use futures contracts to fix the price of the commodity they are purchasing. That reduces their risk that prices will go up. Sellers of these commodities use futures to guarantee they will receive the agreed-upon price. They remove the risk of a price drop.

Buyers and sellers reach a contract price based on current information aggregated about the future value of a commodity. Useful information could include forecasts of possible commodity prices, impacts of war or weather on the quality and quantity of a commodity, government regulations that affect the structure or operation of commodity product or resource markets, or regional or worldwide macroeconomic trends affecting those markets. Prices of commodities change on a weekly or even daily basis, dictating frequent changes in consumer prices of meats, gasoline, and gold. For instance, PJM Interconnection LLC [PJM (2022)]4 applies hourly– (PJM Data Miner, 2022a) and day–ahead (PJM Data Miner, 2022b) markets used to balance the transmission of electric power among electricity users.

Information aggregation and price discovery

Futures markets not only provide practical trading opportunities, but they also demonstrate some interesting and valuable qualities for information aggregation (see Hull (2016) for a review of the operations of futures markets). Economists have long held the belief that markets efficiently collect and disseminate information about goods and services as prices necessary to satisfy both buyers and sellers are discovered. Hayek (1945) generated the hypothesis that, through the price discovery process, markets aggregate the less–than–perfect, diverse information widely dispersed among individual traders and disseminate this information to all traders.

The so–called “Hayek Hypothesis” has empirical support from a series of experiments that have illustrated the dissemination of knowledge from the informed to the uninformed as well as the full aggregation of knowledge among partially informed bidders (Plott (2000) contains a review and summary of the experimental research). Also, the economic theory of rational expectations, originating with Muth (1961) and most closely associated with Lucas (1987), not only acknowledges the information aggregation capacity of markets, but it also the ability of markets to convey information through the price and volume of assets traded.

The information aggregation mechanism first identified by Hayek suggests that markets are the final arbiters of value and that markets provide an excellent method for harnessing knowledge distributed across their participants. Plott and Chen (2002) asserted that business pages of newspapers almost daily interpret market behavior as an aggregation of information about future events. Markets are thought to anticipate changes in price inflation, shifts in federal monetary policy, or prospects for disruptive events like war or labor stoppages. Plott and Chen (2002) further suggested that,

Reflecting on every day notions about the way that people learn from observing other people can form a common sense impression of how an aggregation mechanism might work. For example….if a crowd is observed looking at something then there is a propensity for additional people to look. The actions of the crowd suggest they know something and others instinctively incorporate this possibility into their own information base….”Insiders,” those with bits and pieces of information, those with good “intuition” about events are registering their beliefs through their actions in the markets. That is,…the markets are like a vacuum sweeper, collecting and aggregating information that is otherwise highly decentralized and privately held. (pp. 2–3)

Investment goals

A contract holder sells a commodity to producers at the market price current at the time of delivery. The difference between the price of a commodity when a futures contract was purchased and its market price on the date of delivery equals a gain or a loss for the investor. Traders in future markets are motivated by at least three goals:

profit and speculation—exercising opportunities for a margin of earnings due to price gains over costs of acquiring and holding a futures contract;

hedging—guarding against adverse future price changes by locking in current prices; and

arbitrage—simultaneous purchasing and selling identical, or nearly identical commodities in two different markets in the hope of gaining a profit from price differences.

History and Impact

Commodity futures markets are traced to the Middle Ages when they were developed to meet the needs of farmers and merchants facing risks of price variation of grains due to oversupply or shortage brought on by weather, disaster, war, or politics (Carlton (1984) provides an extended history). Commodities exchanges became formal institutions to act as intermediaries between buyers and sellers. The Chicago Board of Trade and the Chicago Mercantile Exchange were established in the mid–19th century in the United States to make markets for buyers and sellers of commodities. Many new commodity exchanges came into existence subsequently. In 1972, the International Monetary Market was established as a division of the Chicago Mercantile Exchange for futures trading of foreign currencies.

Futures markets are one of the most successful financial innovations for trading commodity assets and financial instruments such as currencies, bonds, or equity and debt options. Futures exchanges smooth the communication between buyers and sellers and provide the conditions and rules for trading, all of which are regulated in the United States by the Commodity Futures Trading Commission.

How Information Markets Function Like Commodities Futures Markets

Common Structure

Information markets operate like commodity futures markets. The asset traded in a commodity futures market is a physical good. As I described, a buyer in the commodity futures market might contract for delivery of 5,000 bushels of No. 2 Yellow Corn next March 1 from a seller. By way of contrast, markets that treat information as an asset to be traded and, as a result, are described as information markets5 Information markets for ideas in the form of propositions use the framework, tools, and methods already available for handling commodity and financial futures.

An information market is an exchange for trading specific propositions describing the occurrence of an event at a subsequent point in time. That is, ideas expressed as clear propositions are the objects traded. An example of a proposition: “Sales of the XYZ Management Adjustment Scale will generate $2 million in revenue by the end of the fourth quarter of 2025.” The price of the shares indicates the likelihood that the market participants believe the proposition is true. The volume of trades reveals the interest that the proposition generates among traders. Price and volume are represent in a price-volume plot as exemplified in Figure 5 for the Fetterman v Oz PredictIt market.

Price discovery

Information markets offer contracts priced between zero and $1.00. The purchasing price shows the likelihood of the realization of ideas. In particular, information trade on propositions about whether events will occur and when. Just as in commodity and financial futures, the price of a proposition:

- Reflects the belief aggregated over traders that the proposition

will be realized.

- Is dynamic because it is updated continuously based on market

activity.

- Is responsive to public information as well as subtle perceptions, inside information, and specialized knowledge of information traders about factors thought to affect the eventual occurrence of an event by a future date. In this way, changes in the price of a proposition reflect changes in market participants’ beliefs based on information aggregated about the likelihood that the proposition will be realized.

The same sort of price discovery occurs in commodity and financial futures markets

Implementation

Information markets and commodities and financial futures markets are mounted on electronic exchanges that operate over the Internet to multiply the reach and speed of market mechanisms to obtain timely information. Information markets commonly use double-auction trading mechanisms (i.e., many buyers, many sellers, one broker). Information markets hold the potential to collect and report information in a continuous stream of activity rather than through periodic or episodic data collection and reporting that is common with survey methods. A desirable feature is that information markets have the potential to provide critical information per unit of time relatively less expensively and simpler than survey methods.

Futures markets are highly regulated in the U.S. Because of the use of actual cash for trading, markets run by PredictIt are under the regulatory purview of the Commodity Futures Trading Commission (CFTC) in the U.S. The CFTC has issued a “no–action” letter to PredictIt stating that as long as the PredictIt markets conform to specific guidelines, the CFTC will take no action against PredictIt. The use of participants’ money is an essential feature of PredictIt markets because, as the old adage goes, no one spends your money better than you do. Due to the actual consequences of loss or gain, participants in PredictIt are stimulated to seek information about the markets in which they participate. zstimulation sharpens the quality of the market price realized for any proposition.

Information Markets, Alive and Dead, That I have Known

To provide examples of the variety of information markets deployed, I describe five information markets. Some of these markets still are working; others are not. I summarize The Foresight Exchange (a wide variety of scientific topics, political campaigns, and natural events), the Iowa Electronic Markets (electoral events), the Hollywood Stock Exchange (box office returns, opening weekend performance, Oscar awards), and TradeSports (mainly sporting events). The most controversial information market, by far, is the Policy Analysis Market.

The Foresight Exchange

The Foresight Exchange (2022) is an example of an information market. The Exchange bills itself as “the place to test your ability to predict the outcome of future events. It is also the place to check the current odds of upcoming events and make your own bets” (Foresight Exchange, 2022). One proposition in the Foresight Exchange, with the ticker name Bush04 (Foresight Exchange, 2000) (Figure 6).

![*Summary of the claim claim that Bush wins the 2000 U.S. presidential election.* <br> (Image from Foresight Exchange [-@foresightexchange2000].)](https://davidpassmore.net/blogd/img/infomarkets/Claimnum.png)

Figure 6: Summary of the claim claim that Bush wins the 2000 U.S. presidential election.

(Image from Foresight Exchange (2000).)

The criterion for judging the claim is shown in (Figure 7).

![*Rule for judging that claim that Bush won the 2000 U.S. presidential election.* <br> (Image from Foresight Exchange [-@foresightexchange2000].)](https://davidpassmore.net/blogd/img/infomarkets/fore_claim.png)

Figure 7: Rule for judging that claim that Bush won the 2000 U.S. presidential election.

(Image from Foresight Exchange (2000).)

Figure 7 is a plot of the price–volume plot for this claim for one particular 100–day period before the United States presidential election, which displays the dynamics of changing beliefs that this claim would be realized. Changes in beliefs in the continuing presidency of George W. Bush are shown through changes in price over time. Correlation of the price series with events surrounding the presidential election campaign could provide insight into causal factors underlying series’ changes.

![*Price plot for the life of the claim that Bush will win the 2000 U.S. presidential election.* <br> (Y--axis is graduated in $0.01 increments. Image from Foresight Exchange [-@foresightexchange2000].)](https://davidpassmore.net/blogd/img/infomarkets/bush2k.png)

Figure 8: Price plot for the life of the claim that Bush will win the 2000 U.S. presidential election.

(Y–axis is graduated in $0.01 increments. Image from Foresight Exchange (2000).)

To give a flavor of the diversity and specificity of topics on the Foresight Exchange, several propositions active during 2022 include:

- An earthquake of Richter magnitude ≥8, with epicenter within 100

miles of (one of the US states) CA, OR, WA, AZ, NV, ID will occur

before the end of 2025.

- By 2025 the Federal government of the United States will have ceased to function as a unified democracy.

- By the end of December 31, 2035, a humanly mobile robot will be in actual use, as a worker in some business use, consumer service, military use, civil service, or scientific capacity.

- Evidence of Extraterrestrial Life, fossils, or remains will be found by 12/31/2050.

Iowa Electronic Markets

The Iowa Electronic Markets (University of Iowa, 2021) are small–scale, online, real–money futures markets in which contract payoffs depend on economic and political events such as elections, companies’ earnings per share, and stock price returns (J. E. Berg & Rietz, 2003; Forsythe et al., 1992). These markets are operated by faculty at the University of Iowa Tippie College of Business as part of their research and teaching mission. Participants buy and sell by opening accounts for a minimum of $5 and a maximum of $500. The markets operate continuously using a double–auction trading mechanism.

The Iowa Electronic Markets allow participants to trade with actual money, as opposed to fictional currency as in the Foresight Exchange. Participants use their funds to buy and sell contracts. Traders, therefore, have the opportunity to profit from their trades but must also bear the risk of losing money. Because of the use of actual cash for trading, the Iowa Electronic Markets are under the regulatory purview of the Commodity Futures Trading Commission in the United States of America, just as PredictIt is. The use of participants’ money is an essential feature of the Iowa Electronic Markets because, as it is with PredictIt markets.

The Iowa Electronic Markets provide relatively accurate forecasts of political election results compared to traditional political polls. Although the comparison with polls might not be entirely fair (J. Berg et al., 2008), the Iowa Electronic Markets have shown no apparent biases and, on average, considerable accuracy for large United States election markets (J. Berg et al., 2003). Presidential election markets performed better than lower-profile congressional, state, and local election markets. Markets with more volume near election time performed better than those with less volume. And, in markets with fewer contracts (i.e., fewer candidates or parties), predicted election outcomes are better than those with more contracts. These attributes are desirable when the relatively high costs of political polls versus the relatively low costs of information markets are considered.

Hollywood Stock Exchange

The Hollywood Stock Exchange is a now-defunct information market structured along the same lines as the Iowa Electronic Markets. The Exchange allowed for trading on securities corresponding to movies (this was called “MovieStocks”), including those in production and in theaters, using fake money called “Hollywood Dollars.” Each movie’s security was liquidated four weeks after the release of the movie for $1 per $1 million in box office gross.

Similar to “MovieStocks,” a “StarBond” represented actors and directors that were traded on the Hollywood Stock Exchange. The price of a “StarBond” reflected the overall star power of the actors and directors as determined by Hollywood Stock Exchange traders, as well as how much money celebrities’ films made at the box office as determined by their trailing average gross (TAG). If a celebrity should have happened to meet the end of a career (death, retirement, etc.), the “StarBond” was cashed out at the TAG.

The Hollywood Stock Exchange was a popular entertainment mechanism. The structure of the Hollywood Stock Exchange was quite sophisticated, with reserve and investment banks, leader boards, trading clubs, tickers, insider trading, funds, options, warrants, and even its own “Hollywood Securities and Exchange Commission.” Based upon the volume of trades and other activities, the Exchange demonstrated how active an information market can become when it captures public interest.

TradeSports

TradeSports was a web-based fantasy sports predictions game (Heitner, 2014) that closed for business in 2015. To classify it plainly, TradeSports was a gambling forum. It was run online from Ireland, so it evaded anti–gambling laws in effect in many countries, such as the United States. What differentiated TradeSports from many other online gambling outlets were the diverse betting topics covered and the use of market mechanisms to operate its betting system.

TradeSports offered quite a diverse betting portfolio. Among the prominent trades available were traditional sports bets (e.g., “Will England win The Ashes 2005?”), contracts related to terrorism (e.g., “Will Osama Bin Laden be captured/neutralized by 31 December 2005?”), and the likelihood of political outcomes (e.g., “Will John Bolton be confirmed by the United States Senate to become the next United States Ambassador to the UN?”). No handicappers were setting the odds for TradeSports bets. Instead, the price was driven entirely by market transactions and self–organized under market principles. Also, TradeSports demonstrated that, given sufficient motivation, many people can be motivated to learn the intricacies of information market trading.

An interesting use of the TradeSports market was in a National Bureau of Economic Research study (Leigh et al., 2003) that noticed a TradeSports market for "Saddam Securities" moved closely with the spot price of a barrel of crude oil. The "Saddam Securities" asset paid off if "Saddam Hussein is not President/Leader of Iraq by [Date]," with the [Date] substituted over various horizons by key contract dates of December 2002, March 2003, and June 2003. Using the specter of Hussein's continuation as Iraq's leader as a proxy for the likelihood of war and disruption in the Middle East, analysts were able to create a derivative security indicating that war could raise oil prices by $10 per barrel, lower the value of United States' equities by 15%, and bolster gold and energy markets.

Policy Analysis Market

One of the most controversial information markets was the quickly–aborted Policy Analysis Market (Wikipedia, 2022)that was sponsored by the United States Department of Defense. The underlying idea for the Policy Analysis Market was to build and test information markets that would allow defense and intelligence analysts to speculate such strategic and geopolitical issues as the probabilities of specific kinds of failure within the national infrastructure of the United States. Its goal was to develop market–based techniques for avoiding surprise and predicting future events.

A now–archived Policy Analysis Market website provided an example of a complex derivative assembled from two idea futures contracts tied to the now–historic case of pending hostilities between the United States and Iraq: (a) whether the Jordanian monarchy would be overthrown during hostilities between the United States and Iraq, and (b) the ability of the Iraqi regime to persist for more than one month of hostilities. A Policy Analysis Market trader who felt comfortable with both issues might choose to trade a contract on a joint outcome, a type of market derivative. Policy Analysis Market held the promise of applications of a variety of similarly rich decision analysis tools associated with joint probability analysis and combinatorial mathematics to anti–terrorism analysis.

The United States Department of Defense canceled the Policy Analysis Market during late 2003 due to the controversial political substance of the speculative propositions that it would consider. U.S. politicians criticized the Policy Analysis Market as more of a “market for death”, “a federal betting parlor on atrocities,” and “an incentive actually to commit acts of terrorism” (Congressional Record, 2003) rather than a decision tool. Abramovicz (2004) opined that the Policy Analysis Market “debacle has provided a setback, maybe a permanent one, to anyone who might have hoped to use information markets in administrative decision–making.” The controversy surrounding the Policy Analysis Market was front–page news in the United States. A member of the United States Senate, Byron Dorgon, asked, “Can you imagine if another country set up a betting parlor so that people could go in…and bet on the assassination of an American political figure?” (Hulse, 2003).

Looney (2004) articulated several arguments offered by counterintelligence agencies against the Policy Analysis Market. The market could incentivize someone to buy futures on a violent act and then carry it out. Markets may be inefficient in the short run, and rumors might be used to manipulate the market. Hansen et al. (2005) noted that, although the Policy Analysis Market was cancelled just one day after it was launched by the Department of Defense, press reports following the cancellation indicated that press reports about the Market became more positive as journalists began to understand its motives and workings.

Some Cautions and Technical Enhancements

Although information markets are capable of aggregating information efficiently, they are susceptible to problems such as market manipulation ((Hanson et al., 2006); (Nöth & Weber, 2003); ) and inability to settle on an equilibrium price ((Anderson & Holt, 1997); (Scharfstein & Stein, 1990)). These problems are exacerbated when traders have limited experience with the information being aggregated in the market and when markets are illiquid (i.e., have few buyers and sellers) (Sunder, 1992).

Chen, Fine, and Huberman (2003) employed Bayesian estimators to integrate prior information about risk aversion into estimates of equilibrium prices in information markets with small numbers of participants. Their process operates in two stages. First, an information market is run to extract risk attitudes from market participants, along with the participants’ ability to predict a known outcome. Constructed from this information about risk aversion is a nonlinear aggregation function that allows for collective predictions of uncertain events. Second, these same participants engage in a market for an uncertain event. Individual market transactions are integrated using the nonlinear function and are used to predict the outcome of the pending event. Use of prior information substantially improved estimates previously obtained solely through the idea futures market for the event. Estimates based on Bayesian nonlinear functions were more accurate than the most accurate individual market traders.

Conclusion

Information markets seem to be a valuable alternative to survey methods for estimating candidate preferences of the electorate, as demonstrated in the information markets and survey-based approaches to following the Fetterman v Oz race. Despite the long history of applications of information markets to information aggregation, pollsters for campaigns seem to prefer survey-based methods.

This posting is a refinement of work published in the Journal of Derivative Markets (Passmore et al., 2005b) and in Human Resource Development Review (Passmore et al., 2005a). Various aspects of this essay were presented at the 4th Annual Irish Technology Users Conference, the 5th International Conference on Information Technology Based Higher Education and Training in Istanbul, Turkey, at the CEO’s Conference on Human Resources Metrics and Analytics sponsored by the Marshall School of Business at the University of Southern California, to the Rocky Mountain Human Resource Planning Society, in the Innovators Speakers Series sponsored by Penn State University, at the Patient–Focused Care Symposium sponsored by the AMD3 Research and Education Foundation and the University of Pittsburgh Medical Center at Magee Women’s Hospital, at the “Thought Leaders Breakfast” at the 2006 Global Conference of the Human Resource Planning Society, and at the annual meeting of the Northeastern Educational Research Association. Over the years, my collaborators in the study of information markets have been Rose M. Baker (2022), University of North Texas, and Evi̇n Doğan Cebici (2021), İstanbul Şişli Meslek Yüksekokulu.

Last updated on

[1] "2022-10-28 10:51:38 EDT"My Approach to the Topic of This Posting: Emphasis on Information Markets; Less Attention to Survey Methods

As I write this posting in August 2022, the U.S. is preparing for the post-Labor Day start in earnest of campaigns for the November midterm elections to public office. I often have wondered why political candidates interested in public opinion levels and variations fail to take advantage of information markets. Although I never have done the calculations, my sense is that the relative cost of information markets compared with conventional surveys per unit of information would favor information markets. I guess you could count me as have a prior bias toward information markets without further data, which is discernible by the amount of emphasis I place in this blog on information markets. What limits the adoption of information markets? I assess that the reluctance to adopt information markets has to do with: (a) wide familiarity with survey reporting from surveys and limited exposure to information markets among clients and media; (b) difficulty in inducting participants into information markets due to relatively small numbers of people who do commodity futures trading (related to point (a)), and (c) sparse software to support implementation of information markets.

Your Comments & Corrections

To make comments about this posting or to suggest changes or corrections, send email to David Passmore, send a direct message on Twitter at @DLPPassmore, or send an IMsg or SMS to dlp@psu.edu.

Reuse

Source code for this blog is available at https://github.com/davidpassmore/blog. Text, illustrations, and source code are licensed under Creative Commons Attribution CC BY 4.0 unless otherwise noted. Any figures/photos/images/maps reused from other sources do not fall under this license and are recognized by text in captions starting: “Figure from…” or “Photo from…” , “Image from…” or “Map from….” Images from external media are framed with with a border. Sources for these external media are cited in captions.

Acknowledgement

The bibliographic assistance of Theresa Thonhauser is appreciated.

See the appendix to this blog posting, “My Approach to the Topic of This Posting,” for my motivations for writing this essay.↩︎

Data for all Senate races in the U.S. are available from fivethirtyeight.com (2022). I extracted data pertaining solely to Pennsylvania and made these state data available for download in a .cvs file.↩︎

Can you imagine investors living in a shady, residential neighborhoods having 5,000 bushels of corn dumped in their front yards on the delivery date specified in their contracts?↩︎

A regional transmission organization in the United States that coordinates the movement of wholesale electricity in 13 of the United States and the District of Columbia.↩︎

Information markets are identified at times as “idea futures markets,” “prediction markets,” or “decision markets” because they are used to assemble forecasts and to align information for decision-making.↩︎